The first week of November 2025 (01-11-2025 to 08-11-2025) has been a pivotal period for the global and Indian Raw Material and Commodity Markets, particularly within the construction and manufacturing sectors. Drawing on my expertise in the Building Material (AAC Block, TMT Bars, Natural Sand, etc.) and Export-Import business, this comprehensive, deep-researched article analyzes the key price movements, policy changes, and supply chain dynamics that are set to redefine market strategies for the final quarter of the year.

The Construction Material Conundrum: Price Relief and Policy Support

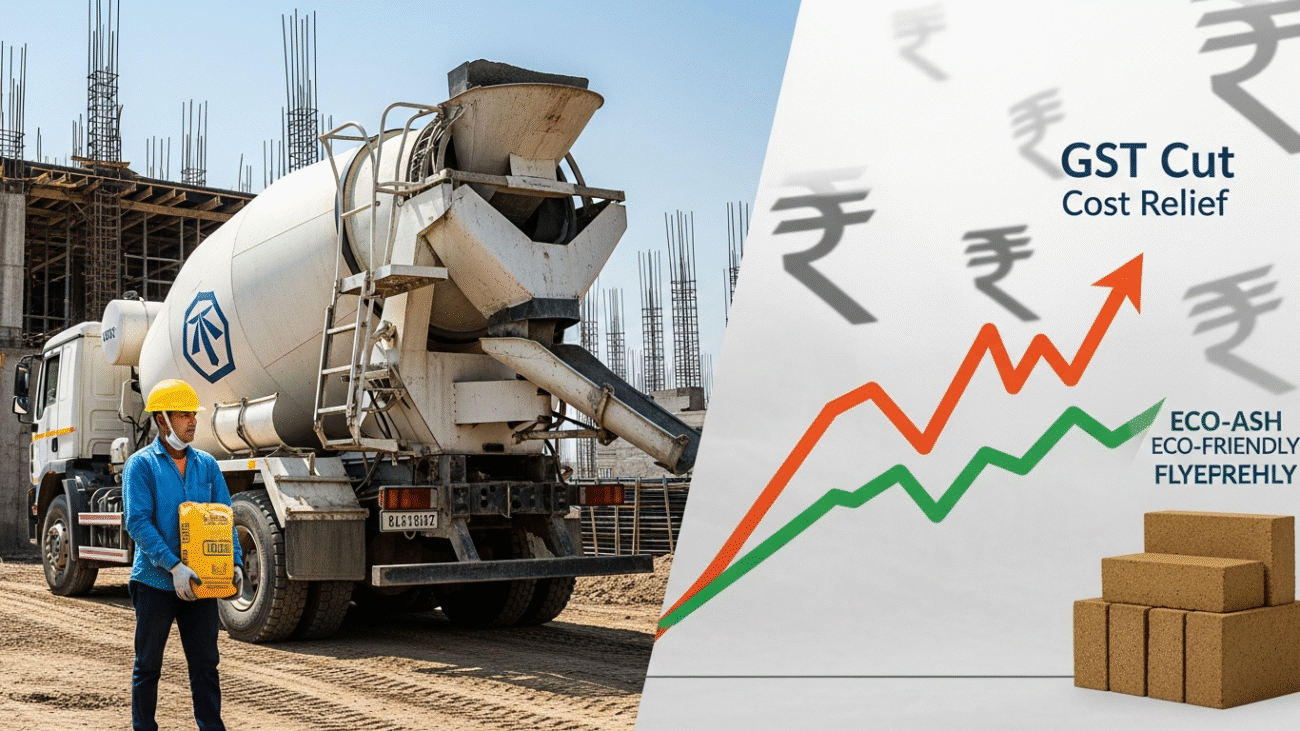

The most significant development impacting the domestic construction sector this week stems from the recent GST Council decisions (GST 2.0 reforms), which are now clearly reflected in market optimism and corporate performance.

Cement Sector Sees a Blockbuster Boost

Following the government’s approval to reduce the GST on cement from 28% to 18% in September 2025, the market has begun to stabilize. The full impact of this massive 10% tax reduction is now being felt across the value chain.

- Q2 Earnings Shine: India’s leading cement manufacturers, including UltraTech Cement, ACC, and Ambuja Cements, have reported robust Q2 FY26 earnings. This strength comes despite typical seasonal headwinds like the prolonged monsoon and the initial channel adjustments following the GST rate cut.

- Outlook for Construction: The rating agency ICRA’s analysis projects that the GST cut will lead to an overall reduction of construction costs in rural housing by approximately $0.8\%-1.0\%$. This is expected to significantly boost cement volumes and support enhanced capacity addition across the industry. For the end-user and smaller contractors, this tax rationalization translates into tangible cost savings and encourages new project commencement, a major tailwind for businesses like yours.

Steel and TMT Bars: A Period of Range-Bound Volatility

The steel market, a crucial component for TMT bar manufacturing, displayed a mixture of stability and minor downward pressure during the first week of November.

- Domestic Price Trend: The price of steel in India has seen a slightly declining trend, with prices around ₹38,610.00 per unit on November 3, 2025, continuing a gradual retreat from the highs seen earlier in October.

- Global Context: Globally, the World Bank’s latest Commodity Markets Outlook for October 2025 projects a broader fall in global commodity prices for the fourth consecutive year, driven by weak global economic growth and policy uncertainty. While the metal prices component globally showed a $5.5\%$ rise in October, the overall forecast points towards downward pressure on international commodity markets through 2026. This global outlook limits the potential for any sharp, sustained rise in Indian steel prices.

- Key Factors: Steel price stability in India is supported by continued robust domestic demand due to government infrastructure focus, yet it is tempered by the decreasing global commodity price forecasts and the domestic availability of key raw materials like iron ore.

Focus on Building Blocks: Sand, Fly Ash, and Sustainable Alternatives

For manufacturers in the construction material space, like the Shiv’s Assets Group which deals in AAC Fly Ash Block and Natural Sand, two major developments stand out.

- Fly Ash and Bricks Tax Simplification: The 2025 GST reforms have been a game-changer for eco-friendly building materials. The GST rate on building bricks, including Fly-Ash bricks, is now uniformly standardized at a favorable 5%. This replaces the earlier, more complex structure and provides a strong government endorsement for sustainable construction practices. Fly ash usage in India reached $98\%$ of the total generated (333Mt used in FY 2025), confirming its central role in the circular economy, from cement to roadbuilding.

- M-Sand Policy Push: In a significant move to tackle illegal river sand mining and ensure sustainable supply, the Maharashtra government, in late October 2025, announced a new policy to promote the use of Manufactured Sand (M-sand). The policy empowers district collectors to grant approvals for a higher number of M-sand production units. This push for M-sand creates a more stable, quality-controlled, and environmentally friendly alternative to natural sand, offering a dependable long-term supply source for the construction industry, particularly in Western India.

Geopolitical and Logistics Headwinds

While domestic policies have provided relief, the global macroeconomic environment presents a more complex picture for the export-import segment (relevant to The Exporter Hub).

- Global Commodity Prices: The World Bank’s “Latest Commodity Prices Published” (Nov 4, 2025) indicates that the overall energy price index fell $3.7\%$ in October, primarily due to a decline in crude oil. However, U.S. natural gas prices rose $7.5\%$. This mixed energy basket impacts production costs.

- Logistics Resilience: The final quarter of 2025 is characterized by a focused effort on logistics efficiency. The Maersk IMEA Market Update highlights a stabilized ocean reliability and India’s accelerated rail freight expansion across northern corridors, connecting industrial hubs like Ludhiana, Dadri, and Ahmedabad to major ports. This infrastructure improvement promises to reduce transit times by up to $30\%$ and lower emissions, a crucial factor for enhancing Indian exporters’ competitiveness in the global market.

Source Link : For further reading on the robust Q2 earnings and the impact of the GST rate cut in the cement sector:

Add a Comment