The week of October 12–18, 2025, brought a mix of challenging headwinds and structural bullish signals across the global Raw Material and Commodity Markets. While precious metals continued their stellar run, a growing sense of caution gripped the base metals sector, primarily due to lingering global industrial weakness. Meanwhile, the building materials market, a key area for The Exporter Hub, showed signs of resilience driven by strong demand in emerging economies like India and a persistent push toward sustainable construction.

Urgent! 5 Metal & Building Price Shifts in Q4 2025

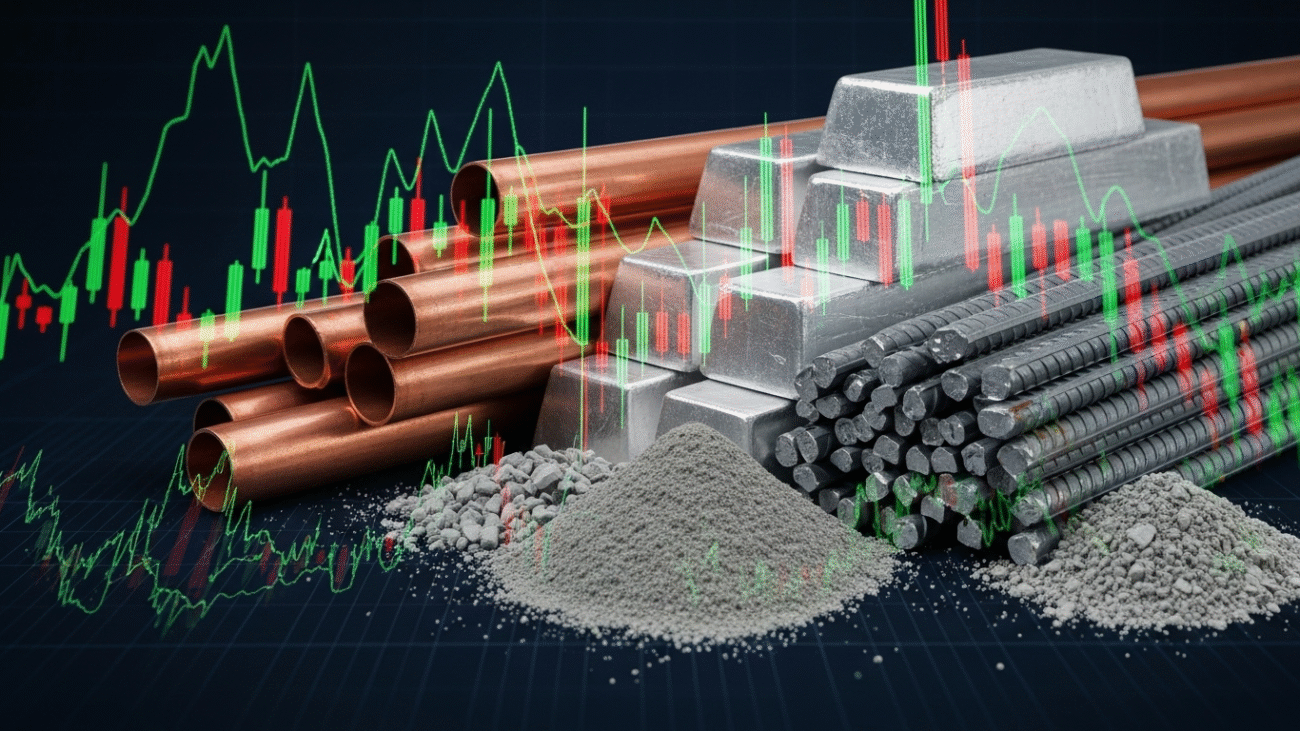

Base Metals: Supply Disruptions VS. Demand Concerns

The industrial metals complex—comprising copper, aluminium, and steel—experienced a tug-of-war between supply-side disruptions, which tend to push prices up, and weaker industrial demand, which weighs them down.

Copper: The Green Economy’s Tight Squeeze

Copper remains a key barometer for global economic health and the energy transition. This week’s movement highlighted its split personality. On the one hand, a major production halt at a key Indonesian mine, alongside general declining ore grades globally, has tightened supply for the immediate term. Furthermore, China, the world’s largest consumer, continues to show supportive demand, often opportunistically buying on dips.

However, the shadow of a global demand slowdown is a significant headwind. Concerns over the lagged impact of monetary tightening and a generally weak global manufacturing Purchasing Managers’ Index (PMI) have tempered the upward momentum. Analysts are forecasting a near-term surplus, with a potential minimum 10% tariff on U.S. copper imports adding to global trade tensions, which could disrupt established trading corridors. Despite this, the long-term outlook remains overwhelmingly bullish, driven by the colossal requirements for EVs, renewable energy infrastructure, and data centers—all requiring massive amounts of the “red metal.”

Aluminium: Output Caps and Strategic Demand

Aluminium saw prices holding firm, close to multi-year highs earlier in the month, though some volatility was observed this week. The key drivers are tight supply and strategic long-term demand. China, in an effort to combat industry overcapacity and manage environmental concerns, cut its annual output growth target for base metals. This cap, alongside the shutdown of a major alumina refinery in Australia due to bauxite grade issues, is reducing global supply availability.

The long-term demand story is now heavily influenced by the digital economy. Corporate pledges for expenditure on new data centers—which are heavy consumers of aluminium—are providing a bullish floor for prices. For exporters, this suggests a continued need to secure raw materials and manage supply chain risks due to structural production constraints.

Steel and Building Materials: Resilience in Infrastructure

The market for steel, particularly Hot-Rolled Coil (HRC), remains constrained by oversupply and subdued demand, especially from the struggling property sector in China. Global manufacturing weakness continues to exert downward pressure on prices.

In contrast, the broader Building Materials Market—including products like AAC Fly Ash Block, TMT Bars, and Joining Mortar (materials central to Shiv’s Assets Group’s operations)—is showing strong structural growth, particularly in the Asia-Pacific region.

- Cement and Fly Ash: The cement fly ash market is projected for steady growth, driven by rapid urbanization and massive infrastructure development in emerging economies like India. Fly ash, as a cost-effective and environmentally favorable alternative, is increasingly in demand for large-scale projects. Exporters need to be aware that the long-term supply of fly ash faces a critical risk: the global decline in coal-fired power generation, which is the primary source of the material. This divergence suggests future market advantages for companies that can secure alternative Supplementary Cementitious Materials (SCMs) or implement advanced fly ash beneficiation technologies.

- Indian Market Strength: India and China are leading the global building materials growth rates, underscoring the vital role of these markets. The overall global building materials market is on track to hit $1.41 trillion in 2025, with new construction projects representing the largest segment of this growth.

Energy and Precious Metals: Geopolitical and Economic Drivers

Crude Oil: The $60 Question

Crude Oil (Brent) prices continued their moderate slide, with some analysts forecasting a drop to around $60/barrel by year-end. Despite geopolitical volatility and ongoing OPEC+ production management, large headline surpluses are being driven by OPEC+ capacity return and a decelerating global oil demand outlook, accelerated by the long-term consumer shift toward Electric Vehicles (EVs). Geopolitical tensions, particularly in the Middle East and Ukraine, remain the primary upside risk to this forecast.

Gold and Silver: Safe Haven Shines Bright

Gold and Silver maintained their strong bull market, fueled by several macro factors: a structurally weakening U.S. dollar, persistent inflation concerns, and significant buying from Emerging Market Central Banks who are diversifying away from the dollar. Silver, in particular, saw amplified momentum this week, with a surge in its lease rate signaling extreme physical market tightness and scarcity, a strong fundamental sign of sustained high prices.

Source: Citi Global Insights

Add a Comment